Temporary Rate Buydown

Temporary Rate Buydown

UWM offers seller-paid and lender-paid Temporary Rate Buydowns to help borrowers lower their interest rate for the first 12 to 36 months of their

mortgage.

HOW DOES IT WORK?

What? Seller concessions can be used to pay the upfront fee with a seller-paid temporary rate buydown. A lender-paid LLPA option can be used to

cover the buydown cost on a lender-paid temporary rate buydown.

Who? Borrowers who have seller concessions or would like to have a lower interest rate in the beginning of their mortgage for a lower monthly

payment. The borrower must qualify with the initial note rate.

PARAMETERS

- Purchases only

- Eligible Products:

- Conventional fixed and ARMs

- Primary and second homes only

- Jumbo 30-Year Fixed Blue, Pink and Yellow

- Primary and second homes only

- Bank Statement 30-Year Fixed Orange

- Primary and second homes only

- FHA and VA

- Primary homes only

- No USDA products

- Not available on manufactured homes

- Conventional fixed and ARMs

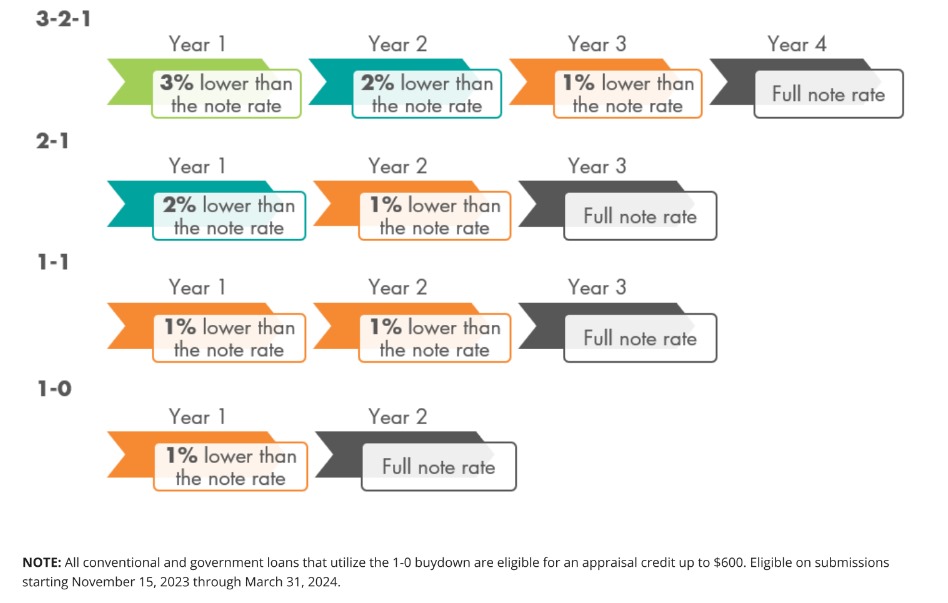

- Buydown Options: 3-2-1, 2-1, 1-1 and 1-0 tiers

- Only the 2-1 and 1-0 options are available on Jumbo 30-Year Fixed Blue, Pink and Yellow and Bank Statement 30-Year Fixed Orange

BENEFITS

- Great opportunity to help sellers get a property sold without affecting the sales price. Great option for when interest rates are high. The benefit goes directly to the borrower

- A great way for borrowers to use any excess seller concessions that often go unutilized. A lower interest rate for the first 1-3 years allowing the borrower to have a lower monthly payment

- Borrower can use the monthly savings to do renovations, upgrades, or buy furniture for the new home

- In a high interest rate environment, borrowers will more than likely be able to refinance to a lower rate than the one they will adjust to after the 1-3 years

- Easier transition from renting to buying by easing the borrower into their mortgage with a lower payment

BUYDOWN OPTIONS

Calculator:

Click here to use the Temporary Rate Buydown Calculator. This calculator will help determine the cost of the buydown. CALCULATION EXAMPLES

Loan Amount: $350,000 / Interest Rate: 5% / P&I Payment: $1,879

3-2-1 EXAMPLE

| YEAR | INTEREST RATE | PAYMENT | MONTHLY DIFFERENCE | ANNUAL SAVINGS |

1 2 3 4

| 2% (5% - 3%) 3% (5% - 2%) 4% (5% - 1%) 5% BUYDOWN AMOUNT

| $1,294 $1,476 $1,671 $1,879

| $1,879 - $1,294 = $585 $1,879 - $1,476 = $403 $1,879 - $1,671 = $208 $0

| $7,020 $4,836 $2,496 $0 $14,352

|

2-1 EXAMPLE

| YEAR | INTEREST RATE | PAYMENT | MONTHLY DIFFERENCE | ANNUAL SAVINGS |

1 2 3 4

| 3% (5% - 2%) 4% (5% - 1%) 5% BUYDOWN AMOUNT

| $1,476 $1,671 $1,879

| $1,879 - $1,476 = $403 $1,879 - $1,671 = $208 $0

| $4,836 $2,496 $0 $7,332

|

1-1 EXAMPLE

| YEAR | INTEREST RATE | PAYMENT | MONTHLY DIFFERENCE | ANNUAL SAVINGS |

1 2 3 4

| 4% (5% - 1%) 4% (5% - 1%) 5% BUYDOWN AMOUNT

| $1,671 $1,671 $1,879

| $1,879 - $1,671 = $208 $1,879 - $1,671 = $208 $0

| $2,496 $2,496 $0 $4,992

|

1-0 EXAMPLE

| YEAR | INTEREST RATE | PAYMENT | MONTHLY DIFFERENCE | ANNUAL SAVINGS |

1 2 3 4

| 4% (5% - 1%) 5% BUYDOWN AMOUNT

| $1,671 $1,879

| $1,879 - $1,671 = $208 $0

| $2,496 $0 $2,496

|

On a seller-paid temporary rate buydown, the borrower can allocate any seller concessions available to cover the buydown fee. The total seller

concessions must be greater than or equal to the buydown amount, and verbiage must be present stating that the seller approves that the seller concessions will cover the buydown.

NOTE: If the property is sold by the borrower and the mortgage is prepaid in full during the buydown period, the non-disbursed and available buydown funds shall be credited to the unpaid principal balance of the mortgage. If a refinance occurs, the buydown funds are held in an escrow account. These funds will be used to pay down the principal of the new loan.

BUYDOWN CHARGE

The buydown charge is auto-calculated as a Temporary Rate Buydown fee in Section H of the Fees screen in EASE.

https://thesource.uwm.com/Search-Guidelines/UWM-Documents/Sales/Sales-Articles-with-UND-Content/Temporary-Rate-Buydown-Sales-UND 3/5

12/5/23, 1:40 PM Temporary Rate Buydown

LENDER-PAID TEMPORARY RATE BUYDOWN

On a lender-paid temporary rate buydown, the lender or the broker can pay for the buydown fee with the option of a LLPA charge. If the LLPA

does not cover the entire buydown cost, seller concessions can be used to cover the remainder.

CONVENTIONAL 16-30 YEAR FIXED, CONVENTIONAL ARM, GOVERNMENT AND JUMBO 30-YEAR FIXED:

3-2-1 buydown 4.500 LLPA

2-1 buydown* 2.375 LLPA

1-1 buydown 1.500 LLPA

1-0 buydown* 0.875 LLPA

* Jumbo 30-Year Fixed Blue, Pink and Yellow and Bank Statement 30-Year Fixed Orange loans are only eligible for 2-1 and 1-0 buydowns

Conventional 8-15 year fixed:

3-2-1 buydown 3.750 LLPA

2-1 buydown 2.000 LLPA

1-1 buydown 1.375 LLPA

1-0 buydown 0.750 LLPA

BUYDOWN CHARGE

The buydown charge is auto-calculated as a Temporary Rate Buydown fee in Section H of the Fees screen in EASE.

UCaaS Pricing

| YEAR | INTEREST RATE | PAYMENT | MONTHLY DIFFERENCE | ANNUAL SAVINGS |

1 2 3 4

| 2% (5% - 3%) 3% (5% - 2%) 4% (5% - 1%) 5% BUYDOWN AMOUNT

| $1,294 $1,476 $1,671 $1,879

| $1,879 - $1,294 = $585 $1,879 - $1,476 = $403 $1,879 - $1,671 = $208 $0

| $7,020 $4,836 $2,496 $0 $14,352

|

The content provided within this website is presented for information purposes only. This is not a commitment to lend or extend credit. Information and/or dates are subject to change without notice. All loans are subject to credit approval. Other restrictions may apply. Mortgage loans may be arranged through third party providers.